"It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way – in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only."

A Tale of Two Cities (1859), historical novel by Charles Dickens, opening paragraph of the novel.

“The European Central Bank has a different task from that of the US Fed or the Bank of England”

Chancellor Angela Merkel.

This week analogy with Charles Dickens' masterpiece, relates to the different stance currently being taken in Europe in relation to what the ECB's role should be in the ongoing Europe sovereign debt crisis. Given recent macroeconomic set of data, for both the US and Europe, indeed we can say we have a Tale of Two Central banks.

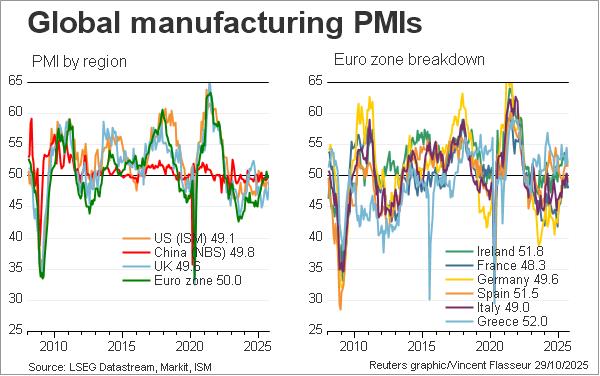

European PMI pointing towards recession:

But I wander again...

Last week, no sooner we had posted a credit update relating to the deterioration of liquidity in the financial system on the 30th of November, that we encountered the mighty coordinated intervention of 5 central banks to unfreeze somewhat a financial system, which is in dire need of dollar support. Well, we already knew from one of our very first credit discussion that liquidity issues always trigger a financial crisis: "It's the liquidity stupid...and why it matters again..." which was in August. We discussed at the time:

"Why liquidity matters again? Because bank funding is a key source for bank earnings, ability to lend, therefore a drag on the economic recovery if it doesn't happen smoothly."

We also noted the following:

"Lack of funding means that bank will have no choice but to shrink their loan books. If it happens, you will have another credit crunch in weaker European economies, meaning a huge drag on their economic recovery and therefore major challenges for our already struggling politicians."

But before we engage in another long credit conversation, revisiting the recent central bank intervention and discussing as well yet another tender, this time around by Lloyds in the UK and the implications, it is time for a quick credit overview.

The Credit Indices Itraxx overview - Source Bloomberg:

The Itraxx SOVx Western Europe index (15 European Western Europe Sovereign CDS) fell towards 328 bps, following the relief rally triggered by the joint intervention of the central banks.

The Itraxx SOVx Western Europe index (15 European Western Europe Sovereign CDS) fell towards 328 bps, following the relief rally triggered by the joint intervention of the central banks.

The Itraxx Financial Senior 5 year index (CDS linked to senior bonds of 25 European banks and insurers) dropped as well below 300 bps to around 285 bps (weekly drop of 72 bps).

My good credit friend commented on the recent price action:

"While the equity market wants to believe in Santa Claus, the credit market does not. I know that credit market participants are often perceived as “negative”. No one seems to remember how positive they have been from 2004 until 2007. Nevertheless, the point is that credit market is the key to the future as the equity market will not perform over time if credit growth does not resume."

The current European bond picture, an impressive relief rally - source Bloomberg:

A significant tightening move as well between the spread of German 10 year government bonds and French 10 year government - source Bloomberg:

German 10 year government yield falling in lockstep with German 5 year sovereign CDS, following the intervention of the central banks - source Bloomberg:

Even our CPDO/EFSF benefited from the fall in European bond yields and fell in conjunction with French OAT 10 year government yields - source Bloomberg:

The somewhat "improved" liquidity picture in four charts. ECB Overnight Facility, Euro 3 months Libor OIS spread, Itraxx Financial Senior 5 year index, Euro-USD basis swaps level - source Bloomberg:

In relation to the acute liquidity issues we have been following, The Economist in their latest publication commented about the intervention of the central banks to ensure a flow of dollars into the system:

"While America has largely escaped spillover from Europe's banking squeeze so far, the shortage of dollars in Europe remains a problem. To relieve that pressure, the Fed lends dollars to the European Central Bank via a "swap" line, which the ECB then lends to its banks, for up to three months. Demand, so far, has been low, because of the stigma for any bank that uses the system, and the cost: 100 basis points more than a benchmark overnight rate.

On November 30th the Fed, ECB and other central banks sought to rectify this by lowering the spread to 50 basis points. Stock markets soared but the euphoria may not last: illiquidity is a symptom of Europe's crisis, not the cause. As long as sovereigns are at risk of insolvency, their banks are, too. If the euro collapses, the resulting chaos will not spare America's economy, despite the health of its banks".

We have discussed at length the issues relating to the oncoming wall of issuance for 2012 for both banks and sovereigns and the issue of circularity, leading to high correlation between both Sovereign credit risk and European banks credit risk.

My good credit friend commented:

"Pro-cyclical austerity budgets will affect a wide range of sectors, and when added to the European banks deleveraging, will have far reaching consequences all over the Globe. Non-financial corporations will not be immune from the slowdown and we should see credit metrics deteriorate further.

The market may breathe better, but health is far from being back. Psychology is key for a recovery, but how will investors react when they will realize that the road to recovery may take years. While US equities are priced for perfection, the risk is for more disappointment."

It brings us back to our "Tale of Two Central Banks" and the European political situation. Germany favors legally binding rules with a possibility to settle cases of fiscal mis-behaving before the European Court of Justice, at the same time President Sarkozy in his latest speech, is ready to crater to German demands of surrendering economic and fiscal sovereignty in exchange for more ECB involvement in helping out on the ongoing European debt crisis. Mario Draghi has also reacted positively to the ongoing French and German conversations: Europe needs a "fundamental restatement of [its] fiscal rules, together with the mutual commitments that euro area governments have made", before the ECB steps in.

We are all awaiting to see the outcome of the paramount meeting of the 9th of December. The most recent interesting proposal in relation to resolving the ongoing European debt crisis has been made by German Finance minister Wolfgang Schauble and the possibility of setting up "redemption funds", in effect pooling sovereign debts exceeding 60% of national GDPs, which would be supported by specific tax provisions and would remain in place for 20 years until all excess debt is finally reimbursed. This proposal was first made by the German Council of Economic Experts.

Credit Agricole Cheuvreux Nicolas Doisy, in his latest Microscope issue published on the 2nd of December entitled - Quantitative Easing euroZone (QE-Z): surviving Near-Death Experience had to say the following in relation to the ECB much needed support:

"Only the ECB has pockets deep enough to ring fence Eurozone sovereigns from market attacks, since Germany is still firmly opposing (i) Eurobonds now and (ii) making the ECB a lender of last resort. Thus, one of the few options for the Eurozone to survive its near-death experience is a QE-Z, i.e. a larger use of the Eurosystem's balance sheet.

Given the risk of governments free-riding such help, Germany is sensibly pushing for a strong safeguard in the form of very strict fiscal discipline through a rapid and limited change to the Treaty. This would limit such a QE-Z to legacy debts on top of the safeguards introduced on 21 July, whereby the EFSF is to conduct government bond purchases at the ECB's initiative and carry the risk.

This would give the ECB full control over its nonconventional

policy within its current mandate, i.e. provide liquidity at longer maturities (2-3 years)and fine-tune it with government bond purchases. This would also maintain sufficient leverage for an efficient use of the carrot & stick approach retained so far to force fiscal and structural reforms. A political accord on tight fiscal discipline at the European Council of 9 December should suffice."

There was as well an interesting rumor about the ECB channeling funds via the IMF which is worth commenting as related by Bloomberg James Neuger on the 2nd of December - Euro Central Banks Seen Providing Up to $270 Billion Through IMF:

"A European proposal to channel central bank loans through the International Monetary Fund may deliver as much as 200 billion euros ($270 billion) to fight the debt crisis, two people familiar with the negotiations said.

At a Nov. 29 meeting attended by European Central Bank President Mario Draghi, euro-area finance ministers gave the go-ahead for work on the plan, said the people, who declined to be named because the talks are at an early stage."

Credit Agricole Cheuvreux Nicolas Doisy commented on the above in his latest article previously mentioned:

"At the same time, informative (and very likely organised) "leaks" let it be known that something involving the ECB to a larger extent was being considered. One such leak was made public by Reuters which quoted un-named Eurozone officials about a "do-able idea": the ECB would lend to the IMF, "to provide the fund with sufficient resources for bailing out even the biggest euro zone sovereigns". Although neither endorsed nor denied by anyone, this "leak" was surely meant to acknowledge the receipt of the markets' demand for larger ECB involvement.

Indeed, it could not be about the IMF, since it would be strange to see the fund put in the very political position of a Eurozone Treasury just when the role of the EFSF was being discussed. The message was rather about securing the ECB’s independence."

We would have to agree with the above analysis. Like any good cognitive behavioral therapist, we tend to watch the process of how and why the message is delivered, rather than focus solely on the content of the message.

Truth is the German's fearful position relating to the ECB is consequent to the rise in ELA (Emergency Liquidity Assistance) in peripheral countries.

And, as Nicolas Doisy interestingly points out:

"The Eurozone's national central banks could go "rogue" and threaten to disorderly run their own quantitative easing."

He also added:

"One major risk arising from a free use of ELA by NCBs (National Central Banks) is a string of disorderly national quantitative easing on the back of free-riding by national governments. Ireland is a living illustration of such a strategy: up until October 2010, the Irish central bank has used ELA generously to keep its banks afloat. It has thus accumulated large amounts of bad assets in return for the commensurate amounts of cash to banks."

As we indicated in August in our post "It's the liquidity stupid...and why it matters again..."

"Conclusion for the banks in the peripheral countries:

The ECB is currently the ONLY SOURCE of wholesale funding for these smaller banks and have therefore prevented aggressive deleveraging to happen and liquidations."

In terms of liquidity issues, there is always what you see, and what you don't see and as Credit-Agricole Cheuvreux Nicolas Doisy puts it nicely in his latest report:

"Indeed, NCBs hold a wild card, as they can provide large Emergency Liquidity Assistance (ELA) at their own initiative and without the ECB's prior consent to their domestic banks. As the name indicates, such ELA is meant to be provided to illiquid but solvent credit institutions shut out of capital markets by exceptional events. Strangely, the NCBs' only legal obligation is to keep the ECB informed."

The Irish stealth QE...ELA as percentage of GDP.

"A year ago, Ireland's ELA operations were revealed suddenly and forcefully by the ECB due to the risk of continued monetary financing of the government. Indeed, the central bank of Ireland was sparing banks the need to restructure by providing them with cheap liquidity. It was thus also indirectly subsidising the Irish government by relieving it from the need to put expensive equity in its banks.

"A year ago, Ireland's ELA operations were revealed suddenly and forcefully by the ECB due to the risk of continued monetary financing of the government. Indeed, the central bank of Ireland was sparing banks the need to restructure by providing them with cheap liquidity. It was thus also indirectly subsidising the Irish government by relieving it from the need to put expensive equity in its banks.

A two-third majority at the ECB's Governing Council would be needed to put an end to such (potentially very large) ELA operations by other NCBs in the future. With much more than one country concerned, such a game of chicken could well turn quickly into a nightmare. Indeed, such a vote would be politically very delicate to hold (the majority threshold is high) and thus likely to trigger panic in the market.

Hence, with contagion spreading to the Eurozone core, a very sensible fear on Germany's side is that monetary financing of fiscal deficit turns widespread. This would jeopardise two pillars of the European Monetary Union: (i) fiscal discipline would be even more relaxed because of the very monetary financing allowed by ELA and (ii) high (if not rising) inflation would eventually ensue from this feedback loop."

source Credit-Agricole Cheuvreux - Quantitative Easing euroZone (QE-Z): surviving Near-Death Experience.

This is the reason Germany is asking for stricter fiscal discipline. A sustainable fiscal federation in the long term is needed of course, backed by a European Central Treasury. In relation to our "Tale of Two Central Banks", you cannot ask the ECB to suddenly morph into a Fed. This process will undoubtedly take time and a due process, but a larger involvement of the ECB is so far conditional to stricter fiscal discipline. Truth is both Germany and France are trying to make amend for their mistake in violating the European Stability Pact in 2003, a subject we discussed in January 2011 in our post "The moral hazard mistake of 2003 - The violation of the European Stability Pact":

"The ECB had to step in and follow a tighter monetary policy.

Between 2003 and 2004 it allowed real interest rates in the Eurozone to fall to zero. The ECB also abandoned the so-called monetary pillar of its strategy -- "a prudent cross-check that looked at the rate at which money supply was growing". For several years, money growth exceeded the ECB's target rate of growth of 4.5 per cent a year. This equated to overreliance on credit in the Eurozone. It made the Eurozone government fiscal balances over dependent on tax revenues from activities that were based on borrowing, namely housing and construction: hence the housing bust in Spain, Ireland, etc."

On another credit note, and in direct relation to our previous warning to subordinate bondholders from our last post, Lloyds, this time around, announced a bond tender on LT2 (subordinate debt), John Glover and Gavin Finch in Bloomberg article - Lloyds Offers to Exchange Up to $7.7 Billion of Junior Notes - 1st of December 2011 indicated:

"Lloyds Banking Group Plc, 41 percent owned by the British taxpayer, offered to exchange as much as $7.7 billion of capital notes for new bonds to boost capital.

Lloyds asked investors in the Tier 2 securities to swap their holdings at a discount to face value of as much as 30 percent, it said in a statement. The transaction will contribute about 20 percent of the bank’s funding needs for next year, according to London-based spokeswoman Nicole Sharp.

“In light of ongoing market volatility and regulatory uncertainty, the group is undertaking an exchange offer on its Tier 2 capital securities which are eligible for call in 2012,” Sharp said in an e-mail. “The exchange offer also provides the group with an opportunity to improve the quality of the group’s capital base.” Regulators are pushing banks to boost their capital, or ability to absorb losses, before taxpayers have to step in. Bank of England Governor Mervyn King urged lenders today to step up efforts to bolster their defenses against the euro area’s debt turmoil, which now looks like a “systemic crisis.” By exchanging Tier 2 notes, banks are getting rid of securities that, under new rules, will start to lose their value as capital notes from 2013. Lenders also get a boost to their capital against losses by swapping the debt at a discount."

Lloyds launched an exchange on all (11 LT2 and 2 UT2) securities with call date in 2012 ("with the exception of those already being treated on an economic basis") into a new LT2 2021 "callable" in 2016 but without step up, coupon range 5yr MS+850-1000bp (depending of currencies) and added "It is the intention of the Group that all decisions to exercise calls on any Existing Notes (the securities targeted in this exchange offer) that remain outstanding after 31 January 2012, will be made with reference to the prevailing regulatory, economic, and market conditions at the time."

Meaning that future calls will be on "economic basis" for the new security. We could summarise the above as follows:

"Dear LT2 subordinated bondholders tender your bonds or the 2012 call gets it, but it doesn't mean the 2016 call won't get it either..."

Oh dear...

Lloyds Isin - XS0195810717 - source Bloomberg, closing cash price before tender 72.2, exchanged price 77.25. A 22.75% "haircut"...

And my good credit friend to opine:

And my good credit friend to opine:

"A nice “slow death” for subordinated bondholders…"

For more on this particular bond tender, FT Alphaville Joseph Cotterill goes into the detail in his post - "Debt swaps: we can do this the easy way or…"

In our previous post we voiced our concern on subordinated bank debt:

"Given the wall of refinancing for banks in 2012 we detailed previously, we would therefore disagree with the current credit market assumption that LT2 haircut will not happen again."

It still looks our concerns are clearly justified.

On a final note I leave you with Bloomberg Chart of the Day showing "Derivative traders are hedging for the risk that European policy makers fail to end the sovereign- debt crisis that a coordinated central-bank move this week to cheapen dollar funding didn’t resolve."

"The CHART OF THE DAY shows that the one-year U.S. interest-rate swap spread rose yesterday following a plunge the prior day after the Federal Reserve and five other central banks cut by half percentage-point the rate on emergency dollar swap lines. The chart also shows that options traders’ projection of the pace of future swap-rate swings is more than 27 percent above the year’s low.

"The CHART OF THE DAY shows that the one-year U.S. interest-rate swap spread rose yesterday following a plunge the prior day after the Federal Reserve and five other central banks cut by half percentage-point the rate on emergency dollar swap lines. The chart also shows that options traders’ projection of the pace of future swap-rate swings is more than 27 percent above the year’s low.

Swap spreads are based on expectations for the dollar London interbank offered rate, or Libor, and are used as a gauge of investor perceptions of banking-sector credit risk. The swap’s floating rate is indexed to three month Libor, which fell yesterday for the first time since July 25."

"Our liquidity is fine. As a matter of fact, it's better than fine. It's strong."

Kenneth Lay - CEO and chairman of Enron from 1985 until his resignation on January 23, 2002.

Stay tuned!

A Tale of Two Cities (1859), historical novel by Charles Dickens, opening paragraph of the novel.

“The European Central Bank has a different task from that of the US Fed or the Bank of England”

Chancellor Angela Merkel.

This week analogy with Charles Dickens' masterpiece, relates to the different stance currently being taken in Europe in relation to what the ECB's role should be in the ongoing Europe sovereign debt crisis. Given recent macroeconomic set of data, for both the US and Europe, indeed we can say we have a Tale of Two Central banks.

European PMI pointing towards recession:

But I wander again...

Last week, no sooner we had posted a credit update relating to the deterioration of liquidity in the financial system on the 30th of November, that we encountered the mighty coordinated intervention of 5 central banks to unfreeze somewhat a financial system, which is in dire need of dollar support. Well, we already knew from one of our very first credit discussion that liquidity issues always trigger a financial crisis: "It's the liquidity stupid...and why it matters again..." which was in August. We discussed at the time:

"Why liquidity matters again? Because bank funding is a key source for bank earnings, ability to lend, therefore a drag on the economic recovery if it doesn't happen smoothly."

We also noted the following:

"Lack of funding means that bank will have no choice but to shrink their loan books. If it happens, you will have another credit crunch in weaker European economies, meaning a huge drag on their economic recovery and therefore major challenges for our already struggling politicians."

But before we engage in another long credit conversation, revisiting the recent central bank intervention and discussing as well yet another tender, this time around by Lloyds in the UK and the implications, it is time for a quick credit overview.

The Credit Indices Itraxx overview - Source Bloomberg:

The Itraxx Financial Senior 5 year index (CDS linked to senior bonds of 25 European banks and insurers) dropped as well below 300 bps to around 285 bps (weekly drop of 72 bps).

My good credit friend commented on the recent price action:

"While the equity market wants to believe in Santa Claus, the credit market does not. I know that credit market participants are often perceived as “negative”. No one seems to remember how positive they have been from 2004 until 2007. Nevertheless, the point is that credit market is the key to the future as the equity market will not perform over time if credit growth does not resume."

The current European bond picture, an impressive relief rally - source Bloomberg:

A significant tightening move as well between the spread of German 10 year government bonds and French 10 year government - source Bloomberg:

German 10 year government yield falling in lockstep with German 5 year sovereign CDS, following the intervention of the central banks - source Bloomberg:

Even our CPDO/EFSF benefited from the fall in European bond yields and fell in conjunction with French OAT 10 year government yields - source Bloomberg:

The somewhat "improved" liquidity picture in four charts. ECB Overnight Facility, Euro 3 months Libor OIS spread, Itraxx Financial Senior 5 year index, Euro-USD basis swaps level - source Bloomberg:

In relation to the acute liquidity issues we have been following, The Economist in their latest publication commented about the intervention of the central banks to ensure a flow of dollars into the system:

"While America has largely escaped spillover from Europe's banking squeeze so far, the shortage of dollars in Europe remains a problem. To relieve that pressure, the Fed lends dollars to the European Central Bank via a "swap" line, which the ECB then lends to its banks, for up to three months. Demand, so far, has been low, because of the stigma for any bank that uses the system, and the cost: 100 basis points more than a benchmark overnight rate.

On November 30th the Fed, ECB and other central banks sought to rectify this by lowering the spread to 50 basis points. Stock markets soared but the euphoria may not last: illiquidity is a symptom of Europe's crisis, not the cause. As long as sovereigns are at risk of insolvency, their banks are, too. If the euro collapses, the resulting chaos will not spare America's economy, despite the health of its banks".

We have discussed at length the issues relating to the oncoming wall of issuance for 2012 for both banks and sovereigns and the issue of circularity, leading to high correlation between both Sovereign credit risk and European banks credit risk.

My good credit friend commented:

"Pro-cyclical austerity budgets will affect a wide range of sectors, and when added to the European banks deleveraging, will have far reaching consequences all over the Globe. Non-financial corporations will not be immune from the slowdown and we should see credit metrics deteriorate further.

The market may breathe better, but health is far from being back. Psychology is key for a recovery, but how will investors react when they will realize that the road to recovery may take years. While US equities are priced for perfection, the risk is for more disappointment."

It brings us back to our "Tale of Two Central Banks" and the European political situation. Germany favors legally binding rules with a possibility to settle cases of fiscal mis-behaving before the European Court of Justice, at the same time President Sarkozy in his latest speech, is ready to crater to German demands of surrendering economic and fiscal sovereignty in exchange for more ECB involvement in helping out on the ongoing European debt crisis. Mario Draghi has also reacted positively to the ongoing French and German conversations: Europe needs a "fundamental restatement of [its] fiscal rules, together with the mutual commitments that euro area governments have made", before the ECB steps in.

We are all awaiting to see the outcome of the paramount meeting of the 9th of December. The most recent interesting proposal in relation to resolving the ongoing European debt crisis has been made by German Finance minister Wolfgang Schauble and the possibility of setting up "redemption funds", in effect pooling sovereign debts exceeding 60% of national GDPs, which would be supported by specific tax provisions and would remain in place for 20 years until all excess debt is finally reimbursed. This proposal was first made by the German Council of Economic Experts.

Credit Agricole Cheuvreux Nicolas Doisy, in his latest Microscope issue published on the 2nd of December entitled - Quantitative Easing euroZone (QE-Z): surviving Near-Death Experience had to say the following in relation to the ECB much needed support:

"Only the ECB has pockets deep enough to ring fence Eurozone sovereigns from market attacks, since Germany is still firmly opposing (i) Eurobonds now and (ii) making the ECB a lender of last resort. Thus, one of the few options for the Eurozone to survive its near-death experience is a QE-Z, i.e. a larger use of the Eurosystem's balance sheet.

Given the risk of governments free-riding such help, Germany is sensibly pushing for a strong safeguard in the form of very strict fiscal discipline through a rapid and limited change to the Treaty. This would limit such a QE-Z to legacy debts on top of the safeguards introduced on 21 July, whereby the EFSF is to conduct government bond purchases at the ECB's initiative and carry the risk.

This would give the ECB full control over its nonconventional

policy within its current mandate, i.e. provide liquidity at longer maturities (2-3 years)and fine-tune it with government bond purchases. This would also maintain sufficient leverage for an efficient use of the carrot & stick approach retained so far to force fiscal and structural reforms. A political accord on tight fiscal discipline at the European Council of 9 December should suffice."

There was as well an interesting rumor about the ECB channeling funds via the IMF which is worth commenting as related by Bloomberg James Neuger on the 2nd of December - Euro Central Banks Seen Providing Up to $270 Billion Through IMF:

"A European proposal to channel central bank loans through the International Monetary Fund may deliver as much as 200 billion euros ($270 billion) to fight the debt crisis, two people familiar with the negotiations said.

At a Nov. 29 meeting attended by European Central Bank President Mario Draghi, euro-area finance ministers gave the go-ahead for work on the plan, said the people, who declined to be named because the talks are at an early stage."

Credit Agricole Cheuvreux Nicolas Doisy commented on the above in his latest article previously mentioned:

"At the same time, informative (and very likely organised) "leaks" let it be known that something involving the ECB to a larger extent was being considered. One such leak was made public by Reuters which quoted un-named Eurozone officials about a "do-able idea": the ECB would lend to the IMF, "to provide the fund with sufficient resources for bailing out even the biggest euro zone sovereigns". Although neither endorsed nor denied by anyone, this "leak" was surely meant to acknowledge the receipt of the markets' demand for larger ECB involvement.

Indeed, it could not be about the IMF, since it would be strange to see the fund put in the very political position of a Eurozone Treasury just when the role of the EFSF was being discussed. The message was rather about securing the ECB’s independence."

We would have to agree with the above analysis. Like any good cognitive behavioral therapist, we tend to watch the process of how and why the message is delivered, rather than focus solely on the content of the message.

Truth is the German's fearful position relating to the ECB is consequent to the rise in ELA (Emergency Liquidity Assistance) in peripheral countries.

And, as Nicolas Doisy interestingly points out:

"The Eurozone's national central banks could go "rogue" and threaten to disorderly run their own quantitative easing."

He also added:

"One major risk arising from a free use of ELA by NCBs (National Central Banks) is a string of disorderly national quantitative easing on the back of free-riding by national governments. Ireland is a living illustration of such a strategy: up until October 2010, the Irish central bank has used ELA generously to keep its banks afloat. It has thus accumulated large amounts of bad assets in return for the commensurate amounts of cash to banks."

As we indicated in August in our post "It's the liquidity stupid...and why it matters again..."

"Conclusion for the banks in the peripheral countries:

The ECB is currently the ONLY SOURCE of wholesale funding for these smaller banks and have therefore prevented aggressive deleveraging to happen and liquidations."

In terms of liquidity issues, there is always what you see, and what you don't see and as Credit-Agricole Cheuvreux Nicolas Doisy puts it nicely in his latest report:

"Indeed, NCBs hold a wild card, as they can provide large Emergency Liquidity Assistance (ELA) at their own initiative and without the ECB's prior consent to their domestic banks. As the name indicates, such ELA is meant to be provided to illiquid but solvent credit institutions shut out of capital markets by exceptional events. Strangely, the NCBs' only legal obligation is to keep the ECB informed."

The Irish stealth QE...ELA as percentage of GDP.

A two-third majority at the ECB's Governing Council would be needed to put an end to such (potentially very large) ELA operations by other NCBs in the future. With much more than one country concerned, such a game of chicken could well turn quickly into a nightmare. Indeed, such a vote would be politically very delicate to hold (the majority threshold is high) and thus likely to trigger panic in the market.

Hence, with contagion spreading to the Eurozone core, a very sensible fear on Germany's side is that monetary financing of fiscal deficit turns widespread. This would jeopardise two pillars of the European Monetary Union: (i) fiscal discipline would be even more relaxed because of the very monetary financing allowed by ELA and (ii) high (if not rising) inflation would eventually ensue from this feedback loop."

source Credit-Agricole Cheuvreux - Quantitative Easing euroZone (QE-Z): surviving Near-Death Experience.

This is the reason Germany is asking for stricter fiscal discipline. A sustainable fiscal federation in the long term is needed of course, backed by a European Central Treasury. In relation to our "Tale of Two Central Banks", you cannot ask the ECB to suddenly morph into a Fed. This process will undoubtedly take time and a due process, but a larger involvement of the ECB is so far conditional to stricter fiscal discipline. Truth is both Germany and France are trying to make amend for their mistake in violating the European Stability Pact in 2003, a subject we discussed in January 2011 in our post "The moral hazard mistake of 2003 - The violation of the European Stability Pact":

"The ECB had to step in and follow a tighter monetary policy.

Between 2003 and 2004 it allowed real interest rates in the Eurozone to fall to zero. The ECB also abandoned the so-called monetary pillar of its strategy -- "a prudent cross-check that looked at the rate at which money supply was growing". For several years, money growth exceeded the ECB's target rate of growth of 4.5 per cent a year. This equated to overreliance on credit in the Eurozone. It made the Eurozone government fiscal balances over dependent on tax revenues from activities that were based on borrowing, namely housing and construction: hence the housing bust in Spain, Ireland, etc."

On another credit note, and in direct relation to our previous warning to subordinate bondholders from our last post, Lloyds, this time around, announced a bond tender on LT2 (subordinate debt), John Glover and Gavin Finch in Bloomberg article - Lloyds Offers to Exchange Up to $7.7 Billion of Junior Notes - 1st of December 2011 indicated:

"Lloyds Banking Group Plc, 41 percent owned by the British taxpayer, offered to exchange as much as $7.7 billion of capital notes for new bonds to boost capital.

Lloyds asked investors in the Tier 2 securities to swap their holdings at a discount to face value of as much as 30 percent, it said in a statement. The transaction will contribute about 20 percent of the bank’s funding needs for next year, according to London-based spokeswoman Nicole Sharp.

“In light of ongoing market volatility and regulatory uncertainty, the group is undertaking an exchange offer on its Tier 2 capital securities which are eligible for call in 2012,” Sharp said in an e-mail. “The exchange offer also provides the group with an opportunity to improve the quality of the group’s capital base.” Regulators are pushing banks to boost their capital, or ability to absorb losses, before taxpayers have to step in. Bank of England Governor Mervyn King urged lenders today to step up efforts to bolster their defenses against the euro area’s debt turmoil, which now looks like a “systemic crisis.” By exchanging Tier 2 notes, banks are getting rid of securities that, under new rules, will start to lose their value as capital notes from 2013. Lenders also get a boost to their capital against losses by swapping the debt at a discount."

Lloyds launched an exchange on all (11 LT2 and 2 UT2) securities with call date in 2012 ("with the exception of those already being treated on an economic basis") into a new LT2 2021 "callable" in 2016 but without step up, coupon range 5yr MS+850-1000bp (depending of currencies) and added "It is the intention of the Group that all decisions to exercise calls on any Existing Notes (the securities targeted in this exchange offer) that remain outstanding after 31 January 2012, will be made with reference to the prevailing regulatory, economic, and market conditions at the time."

Meaning that future calls will be on "economic basis" for the new security. We could summarise the above as follows:

"Dear LT2 subordinated bondholders tender your bonds or the 2012 call gets it, but it doesn't mean the 2016 call won't get it either..."

Oh dear...

Lloyds Isin - XS0195810717 - source Bloomberg, closing cash price before tender 72.2, exchanged price 77.25. A 22.75% "haircut"...

"A nice “slow death” for subordinated bondholders…"

For more on this particular bond tender, FT Alphaville Joseph Cotterill goes into the detail in his post - "Debt swaps: we can do this the easy way or…"

In our previous post we voiced our concern on subordinated bank debt:

"Given the wall of refinancing for banks in 2012 we detailed previously, we would therefore disagree with the current credit market assumption that LT2 haircut will not happen again."

It still looks our concerns are clearly justified.

On a final note I leave you with Bloomberg Chart of the Day showing "Derivative traders are hedging for the risk that European policy makers fail to end the sovereign- debt crisis that a coordinated central-bank move this week to cheapen dollar funding didn’t resolve."

Swap spreads are based on expectations for the dollar London interbank offered rate, or Libor, and are used as a gauge of investor perceptions of banking-sector credit risk. The swap’s floating rate is indexed to three month Libor, which fell yesterday for the first time since July 25."

"Our liquidity is fine. As a matter of fact, it's better than fine. It's strong."

Kenneth Lay - CEO and chairman of Enron from 1985 until his resignation on January 23, 2002.

Stay tuned!

No comments:

Post a Comment